What Can I Do About Inflation? Maybe Hang Onto that Debt!

The information presented in this written blog is the opinion of the author(s) and does not reflect the views of any other person or entity unless specified. The information provided is believed to be reliable and obtained from reliable sources, but no liability is accepted for inaccuracies. The information provided is for informational purposes and should not be construed as advice. Advisory services offered through BRIGHTWORK WEALTH MANAGEMENT, LLC, an investment adviser registered with the state of Colorado.

money at the table

0003 – What Can I Do About Inflation? Maybe Hang Onto that Debt!

25 January 2026

Bottom Line Up Front: If the price of living in the United States has you feeling a little bit helpless, you’re not alone. Indeed – inflation is bad, whether you’re a homemaker or a politician – it just makes you feel like a prisoner. And, like any good prisoner, I’ve spent some time thinking about how to break out…and I wanted to do it through the lens of a question commonly posed – should I buy down some of my mortgage debt by making accelerated payments towards principal?

So - we’ll kill two birds with one stone, here. First, we’ll consider the idea of paying our mortgage lender early – a topic on which you’ll encounter no shortage of opinions at the table. Second – and more conceptually –might we use debt in our battle with inflation??? Let’s dig in.

-------

Background/Overview: What, exactly, is an accelerated mortgage payment? More interestingly – why would you want to do it?

An accelerated mortgage payment, or a pre-payment, happens when a borrower sends an off-schedule, “extra” payment to the lender. This payment, unlike regularly scheduled mortgage debt-service payments, is applied exclusively to the balance (principal) of the loan. In your plain vanilla mortgage contract, this reduction of the outstanding balance will not change the monthly payment, but it will adjust the composition of payments going forward (each remaining payment will be “more” principal than it otherwise would have been, and the mortgage will be paid off earlier). Obviously, the larger the pre-payment amount made today, the greater the impact (the faster the mortgage will ultimately be satisfied).

Why – pray tell – would we do this? Well, here’s a brief list that is not meant to be exhaustive.

Reason: Because we don’t like debt. For many folks, the idea of being debt-free just seems liberating. Because it is. A 30-year mortgage payment comes with 360 payments…and the lender would strongly prefer that you skip none of them – regardless of that month when you lost control of your Labubu habit or (more practically) you had to replace the furnace. Having no mortgage to worry about just feels good, and it certainly brings more flexibility to the family cash flow.

Note: These liquidity considerations are particularly relevant for those approaching retirement, those considering a career change, or anyone for whom ongoing cash outflows might cause problems.

Note1: Beware of your personal feelings when dealing with your money; have your money feelings helped you in the past, or have you been led into trouble. Know thyself😊

Reason: Because I know my return on investment (ROI). If you’re one of those suckers (like me) with a mortgage rate north of 2.25%, you might say – “Hey, if I ‘buy down some debt’ at 6%, I’m making an investment with a guaranteed return of 6% - and that’s not bad.” Note: With Vanguard forecasting 4-5% average annual returns for U.S. stocks over the next 10 years, maybe a guaranteed 6% isn’t so shabby – especially when this “return” isn’t reportable as income.

Reason: Because it really bothers me how much money I’ll pay during a 30-year mortgage. Sometimes, it just hurts when you look at your loan paperwork and realize that your $400,000 home won’t be paid off until you fork over more than $770,000 (assuming a 30-year loan at 6% with a 20% down payment). For some folks, those numbers just make the eyes water, and they get motivated to reduce that total payment number by throwing some extra principal into the mix.

On the other hand – why wouldn’t you want to do this? Well, here’s a brief list that is not meant to be exhaustive.

Counter-Reason: What might you ‘miss out on’ (opportunity cost)? As with any cash-deployment decision, we’ve got to consider if we could do something better. In the case of the mortgage buy-down, we know we could “earn a return” equivalent to our mortgage rate – but what might we miss? For example:

We could invest in public equities (stocks). Historically, long-term ownership in a collection of public companies has outperformed mortgage debt.

Note: This expected outperformance is more likely, all else held equal, over longer time periods.

We could pay down some “high-interest” debt (e.g., credit cards). In this case, we know exactly what our return would be and – in most cases – it’s probably best to eliminate high-interest debt before making an accelerated mortgage payment (today, even creditworthy borrowers are facing credit card rates well over 15%).

We could take a family vacation instead of making an accelerated mortgage payment. Obviously, this isn’t a math question…but we’ve got to recognize that buying down mortgage debt might mean that we’re delaying a consumption goal (e.g., vacation, Porsche, limited-edition Labubu’s, etc).

Counter-Reason: Are you missing out on a larger mortgage expense deduction (on your taxes)? In 2026, the standard deduction remains large by historic standards ($16,600 for single filers, $32,200 for married folks filing jointly) so there’s a pretty good chance you’re not itemizing and not able to deduct mortgage interest expense anyways. But – if you are in the 10% of American families making itemized deductions - we need to run the numbers. Will the benefits generated by an accelerated payment outweigh the benefit of an ongoing tax play?

What’s Inflation Got to Do with It? I freely admit my writing takes a winding path but – at last – we arrive to the thing I’ve been doing some thinking about, having read some stories about postwar Germany. Can regular folks find solace even in something as scary as inflation? Here’s a collection of thoughts:

Inflation in the United States is higher than most central banks would want it to be, and lots of Americans report that it feels even higher than that. You don’t have to be a keen observer of price levels to feel that you’re being squeezed when you look for a home, a load of groceries, or a new (or used) car. Everyone agrees – prices are high and it’s a bummer.

Can we do something about it? Or at the very least – can we feel like we’re doing something?

First, we should acknowledge – if you’ve got a mortgage – you already own a piece of something (the real estate securing the loan) that should be benefitting from the rise in general price levels. Your house is probably worth a lot more right now than it was in 2019. Real estate is oft-cited as an inflationary hedge.

More interesting to me is how your mortgage payment is changing, in real terms. They’re getting smaller. If you’ve got a fixed mortgage, the payments are steady…but inflation makes each one less valuable – which feels good for the payer (you, the borrower) and not-so-good for payee (lender).

I think most folks will agree, once they give it a moment, that their mortgage payments get smaller (in real terms) as time goes on – and that this unique feature of the 30-year fixed rate mortgage in the U.S. can be a powerful tool for a borrower. But do we really integrate this realization into our decision-making (e.g., such as a decision to accelerate our mortgage payments)? Probably not, and for a couple of reasons. The first is that we’re not as rational as we think we are, and certainly not as rational as classical economic models suppose. Note: A good book on the topic is, “Thinking, Fast and Slow” by the late Daniel Kahneman. The second, more tangible reason we don’t appreciate the shrinking of our monthly mortgage payment (in real terms) is that it happens so dang slow.

If you have a father, maybe you were there on the day he “discovered” that a Chevy Tahoe could be sold for $90,000. Or maybe his observation was about some other thing – like a Happy Meal at McDonalds, or a rake at Home Depot. The point is, it’s a dramatic event both because of the righteous indignation reserved for sticker-shocked fathers the world round, and because it’s authentic due to its suddeness. Price changes happen slowly and steadily in reality, but they seem to happen in a stepwise fashion in our brains. And, when the stepwise fashion is increasing the cost of something you “need”, it’s dramatic/painful. Indeed, “high” inflation – or even the perception that inflation is high - keeps central bankers and politicians up at night.

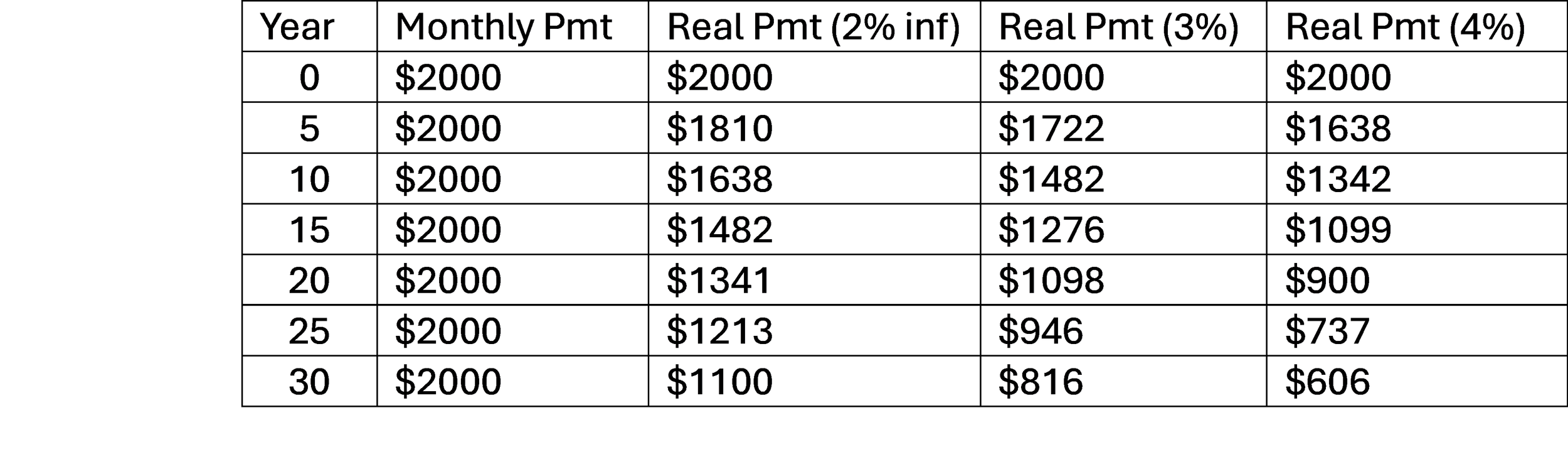

Sadly, this father struggled to “cheer” at the family dinner table when the mortgage payment became just a little cheaper (almost 3% cheaper) in real terms during the past 12 months. Why?!! There’s lots of reasons, of course, but I really want to focus on the speed of change – or lack thereof. While our mortgage stays the same from month to month, the real value of the monthly payment is falling at a very slow rate…so we can’t ‘see’ it clearly enough to include the fact in our intuitive decision-making. If we don’t include the “benefit” of inflation in our decision-making when we contemplate, for example, an early mortgage payment, we’re setting up for a suboptimal decision…at the very least, an incomplete analysis of the decision. Look at this hypothetical case: Assume a 30-year fixed rate mortgage with payments of $2000/mo. In the table’s column 1, you can see how far along we are (in years). In column 2, you can see the nominal monthly payment (it never changes). In columns 3, 4, and 5, we’re adjusting the actual monthly payment downward to describe the future payment in real (present day) terms if assumed rates of inflation are 2%, 3%, and 4% during the life of the loan.

The impact of various rates of inflation (2, 3, and 4%) on “real cost” of fixed-rate mortgage payments.

We can see that mortgage payments are “cheaper” as time passes during the life of the loan, and this effect is magnified when inflation is higher. Shoot – in real terms, your nominal $2000 monthly payment “only costs” you about $1200 in the 25th year of your mortgage (assuming your currency sees 2% target inflation during this loan period). Some follow-on thoughts:

This effect is more relevant if your wages are keeping up with inflation. If your wages are falling in real terms over time, that’s not a great place to be, obviously. But even in that unenviable scenario, at least your mortgage is the one expense you’ve got that isn’t outpacing the growth of your paycheck.

This effect is really relevant for folks who have pensions (like a municipal pension, or Social Security benefits, for example) that are adjusted for the effects of inflation. In that scenario, you’ve got a source of income that is keeping pace with inflation and debt service payments that are falling behind.

Along the way, keep in mind that the asset (your home) is probably appreciating (in the long run, we’d expect a home to keep pace with inflation, at least). So, while the value of the payments are eroding, the value of the asset is probably growing.

Thanks, a lot, Egghead…But What Should I Do? Ok – as we note in our opening disclosure, this blog is designed to inform, entertain, and stimulate folks to feel more confident in their own decision-making, but we can’t give advice through a blog because we don’t have a detailed accounting of the recipient’s personal and financial circumstances. But…

Acknowledge that there is an emotional component to this conversation. If your spouse simply wants the mortgage to be gone, don’t drop an iPad in his or her lap with this fine blog on the screen, step back, and say – “Seeeee????” He or she will probably just get angry with you (your problem) and me (shared problem). Just accept that there is an emotional piece to financial decisions and say, “You’re probably very wise, dear. I thank the stars for you. Let’s just pay that mortgage off.”

If you’ve got a mortgage originated in the glorious (and inflationary) era of 2.5% rates, the household earners are well-insured (life insurance), you’re relatively young, and you expect to earn an inflation-adjusted pension in retirement…you’re a good generic candidate for hanging on to that debt. Tuck yourself into bed at night, smug and snug with the knowledge that you’re doing what you can to fight inflation from the comfort of your fortress.

If you’re heading into retirement with no employer pension and a Social Security benefit on the small-ish side, but maybe you’ve got a bunch of money in your 401(k), IRA, or liquid savings…you might be a good candidate for buying down a little bit of that debt – especially if the rate is a less-glorious (but historically normal) 6% rate. Tuck yourself into bed at night – confident and serene with the prospect of a future with no monthly mortgage payments.

The End: Ok – I feel like I’ve maybe beat this one to death. My apologies. The only thing I want is that you might look at your financial world, and how it interacts with the big financial world, from a number of different and even creative angles. In the case of inflation – which I don’t think is whipped yet – you might find some solace in your situation as the value of your debt-service payments falls. Hey – if central banks can devalue fiat currencies and “inflate their debt away” – why can’t you?

-------

Next month’s post: “Options to Save for Education Expenses”

Have a good topic you’d like to unpack? Have a comment or question from this post or a previous edition? Send us a note through the website (or by writing to chris@brightworkwealth.com or carey@brightworkwealth.com).